Can You Afford to Move Up? The Real Equity Formula for Des Moines Families (2026)

If you bought a starter home in West Des Moines, Urbandale, Clive, or Ankeny 7-10 years ago for around $250,000, you've probably been casually browsing Zillow wondering: "Can we actually afford to move up?"

I help families make this exact transition every month in the Des Moines northwest suburbs, and here's what I can tell you: Most families have built far more equity than they realize. But understanding what that equity can actually buy requires some honest math that most people skip.

By the end of this post, you'll know the real formula for whether you can afford to move up right now—and what your starter home equity can buy in Johnston, Ankeny, or Urbandale.

What Most Move-Up Families Start With

Let's start with a typical scenario.

If you purchased a starter home between 2013-2018, here's what you're probably looking at:

- Purchase price: $180,000 - $280,000

- Current value: $320,000 - $420,000 (depending on location and condition)

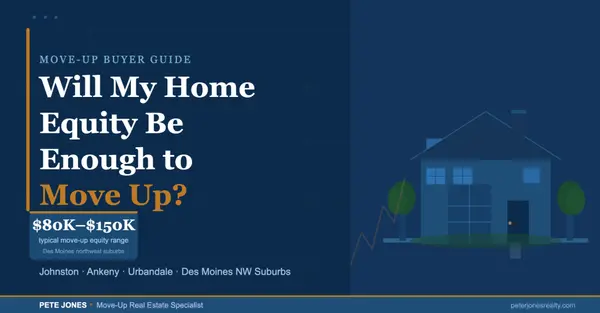

- Typical equity position: $100,000 - $180,000 after mortgage payoff

- Reality check: Most families significantly underestimate the wealth they've built

A Real-World Example

Let's say you bought a 3-bedroom townhome in Clive in 2015 for $215,000. You've been making payments for 9 years. Based on current Des Moines market data, that same townhome is probably worth somewhere between $360,000 and $400,000 today, depending on condition and location.

If you currently owe $190,000 on your mortgage, that means you potentially have $170,000 - $210,000 in equity.

That's a lot more than most families realize they're sitting on.

The Move-Up Formula: What Actually Matters

Here's where it gets real: Your gross equity and your NET equity are very different numbers.

It's not just about how much equity you have—it's about your actual buying power after all costs.

The Math Most People Get Wrong

Let's walk through a realistic scenario:

HYPOTHETICAL SCENARIO:

Starter Home Sale: $380,000

Mortgage Payoff: -$210,000

Sale Costs (6-7%): -$25,000

─────────────────────────────

NET EQUITY: $145,000

Target Home Purchase: $525,000

20% Down Payment: -$105,000

Closing Costs: -$8,000

Cash Reserves: -$15,000

─────────────────────────────

CASH NEEDED: $128,000

REMAINING CUSHION: $17,000The Critical Insight

Here's what's important to understand: If your home is worth $380,000 and you owe $210,000, you don't have $170,000 to work with.

After you pay:

- Real estate commission (typically 6%)

- Closing costs on your sale

- Any buyer-requested concessions or repairs

You're looking at more like $145,000 in net proceeds. THAT'S your real number for planning purposes, not the $170,000 gross equity.

What Your Equity Actually Buys in Each Des Moines Suburb

This is the question everyone wants answered: "What can I actually afford with my equity?"

Let me show you what the current market data tells us. If you have $140,000 in net equity from your current home sale, here's what that realistically positions you for:

Johnston: $500K - $575K Range

With 20% down, you're looking at homes in the $500,000 - $575,000 range.

According to recent MLS data, that gets you:

- 2,400 - 2,800 square feet

- Typically 4 bedrooms

- 3-car garage

- Homes built around 2010 or newer

- Johnston Community School District

- Established neighborhoods with strong resale value

The Johnston Premium: Expect to pay 10-15% more than comparable homes in Ankeny or Urbandale for the Johnston zip code and school district.

Ankeny: $475K - $550K Range

That same equity stretches a bit further in Ankeny.

You're looking at the $475,000 - $550,000 range with similar square footage:

- Often newer construction from 2015-2020

- Modern floor plans and finishes

- Ankeny or Centennial school districts

- More inventory options than Johnston

- Best value proposition of the three districts

The Ankeny Advantage: More housing inventory and newer construction at a lower price point than Johnston.

Urbandale: $450K - $550K Range

In Urbandale, you're typically in the $450,000 - $550,000 range for established neighborhoods.

What you get:

- Homes from 2005-2015

- Mature trees and established character

- More walkable neighborhoods

- Urbandale Community School District

- Best "character per dollar" value

The Urbandale Appeal: Established neighborhoods with character at the most affordable price point of the three top districts.

Current Market Context (January 2026)

What I'm tracking right now: Inventory is still relatively tight in all three areas, especially Johnston. This is affecting how competitive offers need to be and how quickly quality homes are selling.

These price ranges are based on actual closed sales from the last 90 days, not asking prices or wishful thinking.

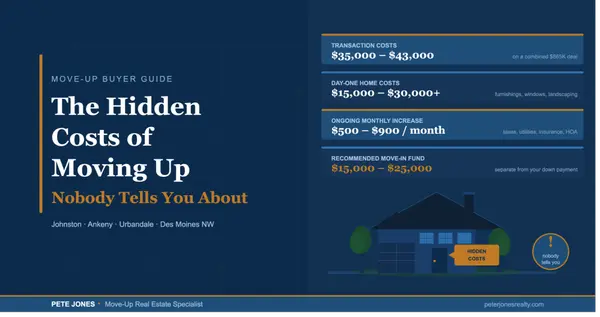

The Hidden Costs Everyone Forgets

Here's what trips people up when calculating whether they can afford to move up.

You think you have $150,000 in equity. But before you even close on your new home:

Pre-Sale Costs

- $4,500 on pre-sale prep: paint, carpet cleaning, landscaping, minor repairs

Sale Transaction Costs

- $23,000 in real estate commission (6% of $380K sale price)

- $2,500 in closing costs on your sale

- $3,200 negotiated in buyer inspection credits (happens more often than not)

Moving Costs

- $2,000 for moving truck, packing supplies, and storage

The Bottom Line

Your $150,000 in gross equity is really about $115,000 in actual cash after all costs.

That's a $35,000 difference from what you calculated on paper.

This is why I always tell families to budget 75-80% of their gross equity as their REAL working number.

Are You Actually Ready to Move Up? The Decision Framework

Here's how I think about readiness. You're truly ready to move up when three things are all true:

Green Light #1: You Have Enough Equity

Generally, that means $100,000+ in NET proceeds after all selling costs. That gives you 20% down on a $500,000 home with some cushion for unexpected costs.

Green Light #2: Your Income Supports the New Payment

As a rule of thumb, if your household income is at least $150,000, you can comfortably afford a $500,000 - $550,000 home.

Run the actual numbers with a lender, but that's a good baseline for the Des Moines northwest suburbs.

Green Light #3: You Have a Clear Reason to Move

Don't move up just because you CAN—move up because it meaningfully improves your family's life.

Valid reasons:

- You've legitimately outgrown your space (kids sharing rooms, no home office, storage issues)

- Your kids need to be in a different school district before middle school

- Your commute or job situation has changed significantly

- You need to be closer to aging parents or family support

Invalid reasons:

- "Everyone else is doing it"

- Fear of missing out on appreciation

- Keeping up with friends or neighbors

Quick Readiness Checklist

✅ Have $100K+ net equity after all costs

✅ Combined household income supports payment increase

✅ Credit score 720+

✅ Clear need (space, schools, location)

✅ Plan to stay 12+ months in new home

If you can check all five boxes, you're probably ready.

The 75-80% Rule: Your Real Buying Power

Here's the formula I give every family I work with:

Take your estimated gross equity → Multiply by 0.75 → That's your REAL working number

Example:

- Gross equity: $160,000

- Real working number: $120,000

- This accounts for all costs, commissions, and cushion

Don't plan your budget on the gross number. You'll end up house-poor or scrambling for cash at closing.

What Happens Next?

If you're a family in the Des Moines metro who bought 7-10 years ago, you likely have $100,000 - $180,000 in equity—possibly more depending on your location and how much you've paid down.

That equity can realistically position you for a $450,000 - $575,000 home in Johnston, Ankeny, or Urbandale, depending on which area you choose and how much you're comfortable putting down.

But remember: Your gross equity isn't your net equity. After commissions, costs, and cash reserves, plan on 75-80% of that number as your real buying power.

Ready to Know Your Specific Numbers?

Every family's situation is different. Your home's value, your remaining mortgage balance, your target neighborhood, and your timeline all affect the calculation.

If you want to know YOUR specific numbers—what your home is worth, what your equity can buy in Johnston, Ankeny, or Urbandale, and whether now is the right time for your family—contact me for a personalized equity analysis.

I'll personally review your situation and send you a custom report showing:

- Current market value of your home

- Estimated net proceeds after all costs

- What that equity can buy in your target neighborhoods

- Whether the timing makes sense for your family

As a move-up specialist serving the Des Moines northwest suburbs, this is exactly what I help families navigate every day—the complete financial picture, not just the fun part of house hunting.

Coming Up Next

In my next post, I'll be covering the 5 mistakes that cost move-up sellers $20,000 - $40,000 when they list their starter home. If you're thinking about selling in the next 6-12 months, you definitely don't want to miss it.

Subscribe to the blog to get notified when new posts go live, or follow me on YouTube where I break down these topics in video format every week.

Pete Jones

Move-Up Real Estate Specialist

Johnston, Iowa | Des Moines Northwest Suburbs

📧 Email Me | 📞 Schedule a Consultation

Specializing exclusively in move-up buyers and sellers in Johnston, Ankeny, Urbandale, Grimes, West Des Moines, Clive, and Waukee.

Categories

Recent Posts

Peter Jones Realty

Phone