Will My Home Equity Be Enough to Move Up in Des Moines?

Why Move-Up Buyers in Des Moines Overestimate Their Equity

Your Zillow estimate says your home is worth $340,000. You owe $195,000. You do the math: $145,000 in equity. That should be more than enough to move up to a 4-bedroom home in Johnston or Ankeny, right?

This is the most common miscalculation move-up buyers make — and it can derail the entire process if you catch it after you're already emotionally attached to your next home.

I specialize exclusively in move-up transactions in Des Moines' northwest suburbs — Johnston, Ankeny, Urbandale, Grimes, West Des Moines, Clive, and Waukee. Here is what your equity actually looks like after the transaction.

What Is the Difference Between Equity and Net Proceeds?

Your home equity is not your take-home amount. Before you see a dollar from your home sale, the following costs are deducted:

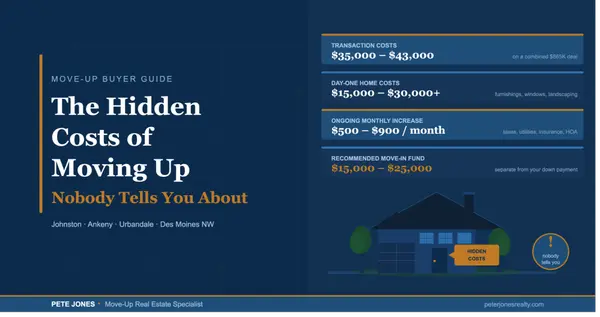

- Agent commissions: typically 5–6% of the sale price

- Seller closing costs: title fees, transfer taxes, prorated taxes — approximately 1–2%

- Repair credits or concessions negotiated during inspection

- Your remaining mortgage payoff

On a $340,000 sale with $195,000 owed and 7% total selling costs, your net proceeds are approximately $119,200 — not $145,000. That $25,800 gap is real money when you are planning a $525,000 purchase.

How Far Does $115,000-$120,000 Go in Johnston, Ankeny, and Urbandale?

Move-up homes in Des Moines' northwest suburbs — 4 bedrooms, 3-car garage, top school district — are currently priced between $425,000 and $650,000. Here is what your net proceeds need to cover on the buy side:

- Down payment: 10-20% of the purchase price. On a $525,000 home: $52,500-$105,000

- Buyer closing costs: 2-3% of purchase price. On a $525,000 home: $10,500-$15,750

- Post-close cash reserves: lenders typically want 2-3 months of mortgage payments in reserve

For most move-up families in Des Moines earning $150,000-$250,000 combined, $115,000-$120,000 in net proceeds comfortably covers a 10-15% down payment plus closing costs on a $475,000-$575,000 purchase — especially when income supports the larger mortgage.

Three Factors That Determine How Far Your Equity Goes

- How Strategically Your Current Home Is Priced and Marketed

My background is 20 years of marketing for major corporations. That expertise directly impacts your net proceeds. Strategic preparation and positioning can add $15,000-$30,000 to a $340,000 sale. That is the difference between a 10% and a 15% down payment on your next home.

- Which Neighborhood You're Targeting

Johnston commands a premium. Certain Ankeny neighborhoods offer equivalent schools at lower price points. If your equity is tighter, I can identify which pockets of the northwest suburbs give you the most home for your money without sacrificing school district priorities.

- Current Interest Rates and Your Mortgage Payment

The difference between a $400,000 and $450,000 mortgage at current rates is approximately $300/month. Knowing this before you start touring homes is essential — it shapes which price range actually works for your family's monthly budget.

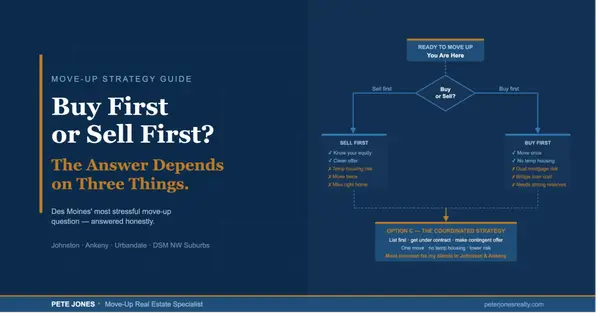

What to Do Before You Start Browsing Zillow

The move-up families who have the smoothest experiences always run the real numbers first — before they fall in love with a specific house in a specific neighborhood. Here is the correct sequence:

- Get a precise market valuation of your current home from a local specialist (not Zillow)

- Calculate your realistic net proceeds after all selling costs

- Determine your maximum comfortable purchase price based on income and payment

- Identify the gap your equity needs to cover on the buy side

- Then begin browsing listings with a clear, accurate number in hand

If the numbers work, great — we build a strategy. If they do not work yet, I will tell you. Coming back in 12 months with more equity is a better outcome than overextending now.

About Pete Jones: Move-up specialist serving Johnston, Ankeny, Urbandale, and Des Moines northwest suburbs. Former marketing executive. Johnston resident and dad of three. Member, Johnston Rotary and Chamber of Commerce.

Ready to take the next step? Contact Pete Jones to run your equity analysis before you start shopping. peterjonesrealty.com

Frequently Asked Questions

How much equity do I need to move up to a bigger home in Des Moines?

Most move-up buyers in Des Moines need $80,000-$150,000 in home equity to comfortably move up. After selling costs of 7-8%, your net proceeds fund your down payment, closing costs on the new purchase, and cash reserves. A move-up specialist can run your specific numbers in a free equity analysis.

What is the difference between home equity and net proceeds?

Home equity is your home's market value minus your remaining mortgage. Net proceeds are what you take home after paying agent commissions (5-6%), seller closing costs (1-2%), and any repair credits. On a $340,000 sale, gross equity of $145,000 typically yields net proceeds of $115,000-$120,000.

Can I use home equity to buy a bigger house without selling first?

Yes. A bridge loan or home equity line of credit (HELOC) allows some buyers to access equity before selling. However, most Des Moines move-up buyers coordinate the sale and purchase simultaneously, using net proceeds from the sale as the down payment on the new home. A move-up specialist and lender can help you determine which approach fits your financial position.

Is now a good time to move up in Des Moines given current home prices?

Move-up buyers in Des Moines are partially hedged against market conditions because they are selling and buying in the same market. If prices soften, your sale price drops — but so does your purchase price. For families planning to stay in their next home 10-15 years, life stage factors (schools, space, community) typically matter more than short-term market timing.

Quick Answer: Will my home equity be enough to move up in Des Moines?

Most Des Moines homeowners who purchased 7-12 years ago have built $80,000-$150,000 in equity — typically enough to move up, but not always as much as you think. After selling costs (7-8% of sale price), your actual take-home (net proceeds) is $20,000-$30,000 less than your gross equity. Running a real equity analysis with a move-up specialist before browsing listings prevents costly surprises.

Categories

Recent Posts

Peter Jones Realty

Phone